Powell vs. Reality: Why the Federal Reserve Will Step In to Save Markets

The market mood has been dark lately. Stocks have cratered. Bonds have crumbled. Consumer confidence is collapsing. And yet, in the midst of one of the fastest 20% market drops in modern history, Federal Reserve Board Chair Jerome Powell essentially told investors yesterday: “We’re in no rush to cut rates.”

That’s right. With the economy cracking under the weight of a global trade war and sentiment falling off a cliff, the captain of the monetary ship looked us in the eye and said, “We’re going to wait and see.”

Wall Street didn’t like it. Stocks and yields initially sank in response.

But we’re here to tell you, don’t panic just yet. More importantly, don’t listen to the words; watch the feet.

Powell may have said “no cuts for now,” but the evolving reality on the ground says something very different…

In fact, we believe the Fed is on the brink of launching a full-blown rescue mission for the U.S. economy – and it could send stocks soaring.

Let’s break it down.

Powell’s Stagflation Dilemma and the Federal Reserve’s Tough Choice

To us, Powell’s message yesterday made clear that the Fed is confused.

He said that Trump’s massive tariff regime is larger than expected and that it will likely create more inflation and slow the economy more than expected. That’s a problem because rising inflation + falling growth = stagflation.

That would be an economy where central banks are damned if they do and damned if they don’t.

Should they raise rates to fight inflation or cut them to combat the slowdown?

Powell said the Fed doesn’t know which it’ll be yet – so it’s going to sit on the sidelines and wait to find out.

That might sound measured and diplomatic. But in reality, it’s a dangerous game of chicken. And Powell knows it.

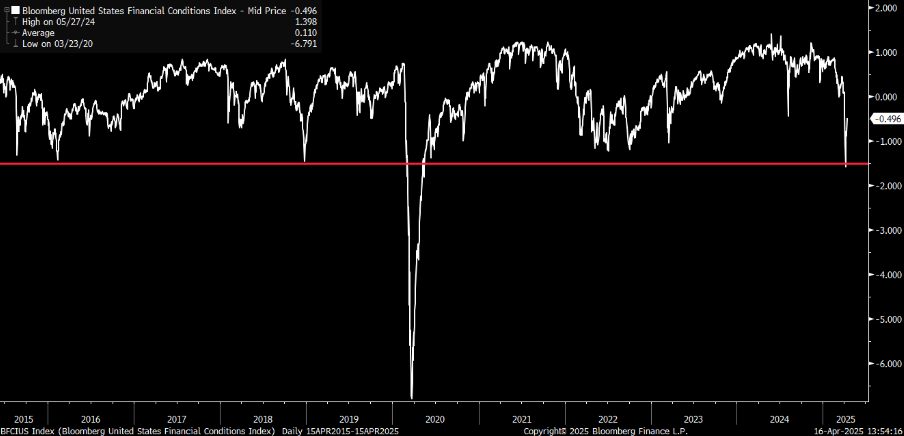

Why the Fed Must Act: Financial Conditions Are Too Tight

If you strip away the ‘Fed speak’ and look at the data, the picture becomes clear: The central bank should already be cutting rates.

Bloomberg’s U.S. Financial Conditions Index – a catch-all measure of credit spreads, equity levels, and money supply – shows that outside of 2020’s COVID crash, financial conditions are now tighter than they’ve been at any time in the past decade.

Indeed, they are currently tighter than they were during China’s 2015 slowdown, the 2018 Fed freak-out, and 2022’s inflation panic.

Financial conditions are too tight…

Because here’s the backdrop we are dealing with right now:

- Consumer confidence is near a 50-year low. According to the University of Michigan’s latest survey, consumer sentiment plunged 11% this month to 50.8 – a 12-year low and the second-lowest level on record since 1952.

- Retail sales are slowing, especially on a core basis. Though sales surged 1.4% in March, this uptick is likely temporary as consumers attempt to ‘frontload’ tariffs. In February, retail sales rose 0.2%, much lower than the 0.7% increase economists projected.

- Business investment has stalled, down $130 billion from Q3 to Q4 of 2024.

- The housing market is frozen solid. Data from the National Association of Realtors shows that existing home sales fell 1.2% year-over-year.

- Despite all of the above, bond yields are spiking, not falling. The 10-year now sits at 4.29%, above where it was before Trump’s “Liberation Day” announcement.

This is not a good cocktail.

It practically screams for Fed action. And we believe Powell is quietly preparing for that – regardless of what he’s saying in public.

Inflation Fears Are Overblown

Now, yes, there’s one reason the Fed has been sitting tight: inflation.

Tariffs could cause reinflation. And the Fed doesn’t want to be cutting rates right as inflation starts running hot again. That’s understandable… in theory.

But in reality, this inflation threat is probably overblown. After all:

- CPI inflation is currently running at 2.4% – very close to the Fed’s 2% target.

- Core CPI inflation is at 2.8% and falling.

- Producer prices and import/export prices are all showing cooling trends. Data from the Bureau of Labor Statistics shows that U.S. import prices decreased 0.1% in March following a 0.2% increase in February. Similarly, PPI for final demand decreased 0.4% in March, goods declined 0.9%, and services fell 0.2%.

Yes, tariffs may cause a temporary blip in inflation. But the Fed knows better than to base long-term monetary policy decisions on short-term price distortions. It’s said as much in the past.

And when you weigh the risks – a modest, short-lived inflation bump versus a full-blown economic breakdown – we think Powell will ultimately choose growth.

When Will Powell and the Federal Reserve Step In? The Likely Rescue Timeline

So, when does the cavalry arrive?

We think it’s coming in June.

That’s when the data will likely have piled up just enough to give Powell and his colleagues the political and academic cover to start cutting. We expect that by then the trade war will likely be cooling (more on that in a second), inflation fears will be abating, and markets will be loudly begging for help.

Our base case is a rate cut in June, preceded by strong forward guidance in the Fed’s May meeting. In fact, we wouldn’t be surprised to hear ‘the pivot’ begin as early as next month.

And when that happens…

The markets will move.

The Cooling Trade War Is a Catalyst

Of course, this Fed story is only half the equation.

The other half is the global trade war — which, we’re happy to report, appears to be losing some steam.

Since the U.S. launched its “Liberation Day” tariffs in early April, we’ve actually seen tariff rates fall, not rise.

The average U.S. tariff rate spiked from 2.5% to 27% on April 2. But with the 90-day pause and electronics exemptions, that number has already fallen to about 23%.

If rumored auto parts exemptions come to fruition, we’ll drop to ~20%. And if steel/aluminum or China deals are locked in, we’ll slide closer to 10%.

That’s a pretty sharp reversal.

Yes, the rhetoric from Washington is still aggressive. But as with the Fed, actions speak louder than words. And right now, the actions suggest deescalation.

That’s very bullish.

Once Powell and the Federal Reserve Pivot, Stocks Could Soar

Put it all together:

- The Fed is almost out of excuses. The data says cut. And it likely will soon.

- The trade war is beginning to abate, and tariff rates are falling.

- Financial conditions are too tight and about to loosen.

- Inflation is easing, not surging.

- And innovation – especially in the AI industry – continues to march forward.

The storm clouds are still thick today. But if you know where to look, the sun is already peeking through.

We believe that as these two macro levers – monetary policy and global trade – begin to shift, the stock market could rip higher. We wouldn’t be surprised to see the S&P 500 up 10% to 15% from current levels by late summer.

So, while others panic, we’re getting ready to pounce.

Now, we’re not saying the road will be easy. There will be more volatility, headline noise, and stock market drops.

But with the Fed about to step in, the trade war thawing, and the AI revolution continuing to accelerate…

This is a time to be disciplined, strategic, and optimistic.

Buy the dip. Own the future. The rescue is coming.

If you’re looking to make the most of it, consider buying AI 2.0 stocks on this recent dip.

We’re talking AI that can respond to real-world environments; embodied intelligence that can see, hear, walk, talk, lift, carry, organize, fix, learn…

After all, there’s a reason why every tech titan is suddenly obsessed with humanoid robots.

That’s where we believe the next trillion-dollar investment opportunities will be found. And we’ve found a compelling way to play that next phase of the AI Boom.

Uncover the details on our favorite AI 2.0 pick.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Questions or comments about this issue? Drop us a line at langofeedback@investorplace.com.